I wrote this newsletter a couple of years ago and I thought it would be worth revisiting. We’ve heard a lot about home construction and building costs increasing sharply after the supply chain and labor shortage issues that COVID has caused. It’s likely that many of our clients should consider reviewing and possibly updating their homeowner's insurance policy due to this increase in re-build costs.

Read on below to learn about 6 times that it might make sense to increase your homeowner's insurance coverage and also for more info about when to check in with your insurance agent on your home’s rebuild/replacement cost. Happy reading!

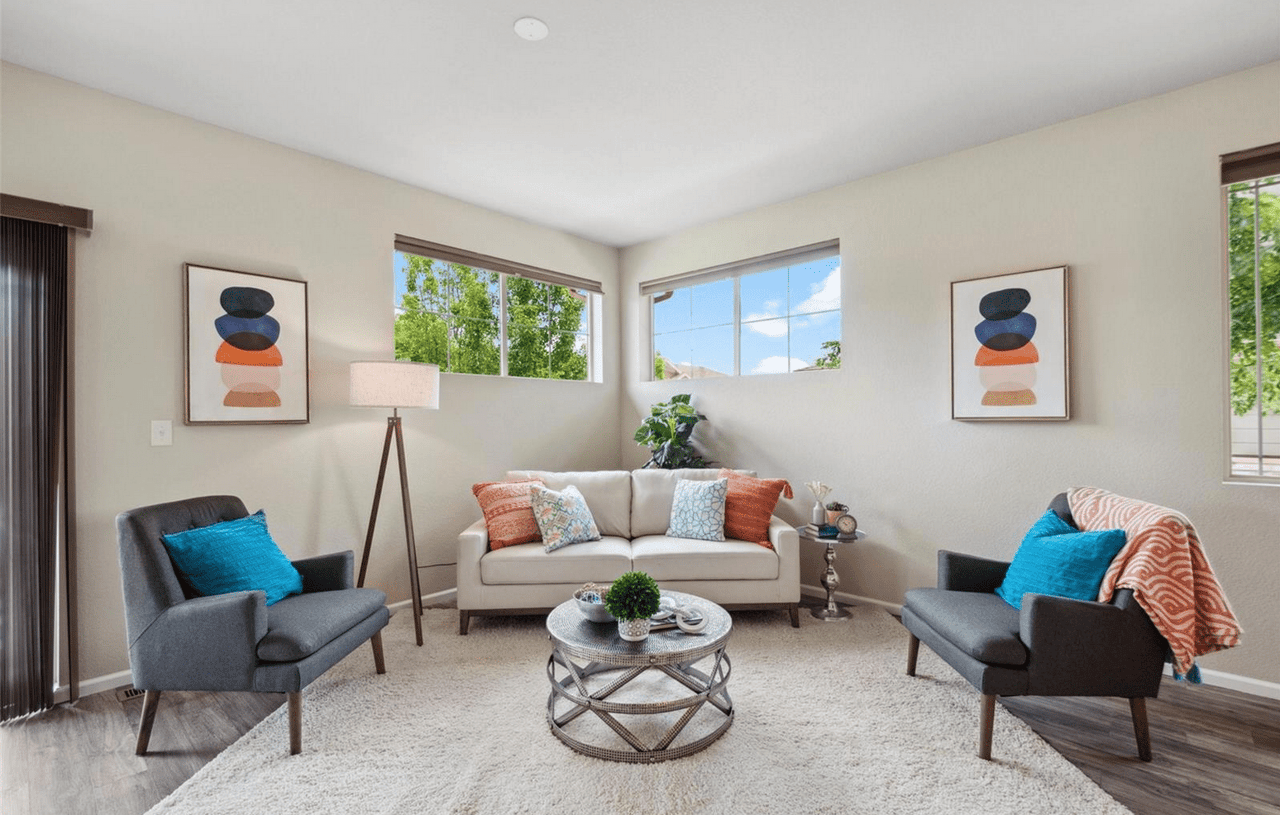

One of the things that most of us put on auto-pilot after we purchase a home is our homeowner's insurance policy. Most of the time people assume that what once worked well in terms of homeowners insurance coverage will always meet our coverage needs. But did you know that there are some key times that we should be reaching out to our trusted insurance advisor to ensure that our homes are insured adequately?

Read on to learn about 6 times when it might be time to re-up on your coverage.

First things first, homeowners insurance covers the insured home’s replacement cost. That means that in the case of a loss or incident, homeowners insurance would cover the cost associated with rebuilding the structure. Over time, this rebuild cost goes up as the cost of labor and materials increases with inflation. Most homeowners insurance policies take this inflation into account and incorporate a modest increase in coverage each year.

However, according to Steve Hakes with Rocky Mountain Insurance Center, this increase doesn’t always accurately reflect the reality of what the rebuild cost could be. Sometimes the index that insurance companies use to automatically increase their coverages could fall behind, especially in our market where contractors can charge such a premium for their services. Steve recommends that homeowners should reach out to their insurance agent every 2 to 3 years to have the rebuild cost of their homes checked manually against the index.

Besides this check-in every 2 to 3 years, there are some other times when homeowners should reach out to their agent to see if increased coverage is necessary.

- When Adding an Addition

If homeowners add on to the structure of their home they should consider increasing their insurance coverage. Whether that addition is a second story, a new finished sunroom on the back of the house, or a new garage, that addition will substantially increase the rebuild cost of the home.

- When Adding Finished Square Footage

This could be an easy one to overlook. Homeowners should remember that if they add finished square footage, they should bump up insurance coverage. The most common time this could come up is if a homeowner finishes their basement.

Steve Hakes added that homeowners should remember to increase coverage even if they don’t finish their basements in full. Also, they shouldn’t forget to increase coverage to account for the possible back-up of sewers, drain lines, and sump pumps into their newly finished space.

- When Substantially Increasing the Value by Improving the Home

If homeowners do tons of nice remodels or flip a property from “builder grade” materials to a more custom property, those things could substantially increase the rebuild cost of a home.

- When Turning Your Primary Residence Into a Rental

When homeowners make their primary residence a rental property, they should take out a landlord policy on that home. Landlord policies are typically more expensive because incidences and losses are more likely to happen at homes that are rented out. Also, landlord policies typically carry higher coverage for liability, as well.

- When You Have a Home Built Earlier Than 1980

Older homes have a higher rebuild cost and this cost goes up faster over time as municipalities update their building codes and add new ordinances. Again, Steve Hakes said homeowners who have older homes should consider upping their Ordinance and Law Coverage. That way, if a loss does occur and a homeowner needs to rebuild some or all of their home, that insured home has higher coverage to account for the fact that some of its components were out of date and need to be redone, not just to the standard it was before the incident, but the home would need to be improved to a higher standard to account for the more stringent, current building codes.

- When You Own a Condo

Many homeowner’s associations have had to change their master insurance policies in the last couple of years and they have moved from having fixed, lower deductibles to deductibles based on a percentage of any claims they make. This can translate to much higher costs for them in the instance of a loss and these costs are more and more often being passed on to condo owners in form of special assessments. Owners of condos (whether they are owner-occupied or rented out) should contact their insurance advisor and consider adding Loss Assessment Coverage. This additional rider is quite inexpensive and could cover condo owners in the instance of a loss and ensuing special assessment levied on the property.

As always, if you have more questions, don’t hesitate to reach out! Until next time!

- Allison Benham and Ken Crifasi with K&A Properties